As we continue our 30,000 feet overview of Economics and terms we have a couple sets of paired ideas to consider. With the idea of scope in mind, we use Macroeconomics to examine the economy as a whole. It is the big picture that encloses everyone and everything as a single chunk. Microeconomics looks at an individual entity and it’s interaction with the greater economy. It could be an individual, household, company, or governmental unit in view when we examine their decisions and the consequences of the same.

Our analysis of actions and consequences can be viewed from different points of view. When we analyze actions with the mind-set that this is “how things SHOULD work” we are doing Normative Economics. Using the view of “this is how things ARE working” we refer to this as Positive Economics. These views are not necessarily the same, and one is not necessarily “better” than the other. Both types of analysis have their uses and each carries its own powers and pitfalls.

As it would be impractical (impossible, really) to interview every person or monitor every transaction in any realistic economy, we use a Model to simplify our work. It is a smaller or simpler representation of a system created to simplify analysis. It will keep the essential parts of a system and minimize (or ignore) unnecessary elements not being studied. A model is created (or designed) to build a framework in which to demonstrate and test a Theory, formally defined in my notes as “a simplified, logical story based on positive analysis that is used to explain an event.” (It should be noted that I found my teaching notes; I did NOT find my text book the notes came out of. I may refer to my copy of The Essentials of Macroeconomics I from Research and Education Association, ISBN 0-87891-700-4 for additional information and will identify anything thus sourced with the marker [REA].)

The method presented in class for creating and evaluating concepts was to use the Scientific Method, a five (5) step process:

- Recognize a problem or issue

- Make needed Assumptions (conditions accepted as true without justification or proof)

- Develop a model based on selected system and assumptions

- Present a Hypothesis (statement that explains a set of facts and action->consequence chains) to describe the analysis

- Test hypothesis for validity (whether the model and theory works or not)

To see how this works, we could setup an example. While working on my blog my pencil rolled off the table and fell to the floor (a couple of times, actually). Since nothing else has fallen off the table, I suspect gravity in my apartment has a special affinity for pencils (step 1: recognize issue). I will assume there are no other forces (wind, telekinetic psychics, or poltergeist spirits) at play here (step 2). I went into the kitchen and cleared the table to use as a model of my desk (step 3). My hypothesis is that pencils are more likely than other objects to fall to the floor (step 4). I then set a number of different objects on the table to see if they would roll off and fall to the floor:

Since other objects than the pencil fell, I must accept that the hypothese is not valid (and now I have a real mess to clean up in the kitchen).

A couple of common mistakes in creating hypotheses to watch out for is the Fallacy of Causation (“since this implies because of this,” just because two things happened together one causes the other) and the Fallacy of Composition (“what one does all do,” or just because Bert puts ketchup on his ice cream, everyone does…or should). My example failed on the falacy of causation.

When we are dealing with models and analysis a critical concept we need to keep fully aware of is that of Ceteris Paribus (Latin for “all other things being equal”). It is used when we make a claim explaining an event (if price for a good goes up, demand will go down [CP]) so that the ONLY thing changing is the item being examined (price). The idea is to eliminate or ignore everything else that might have an effect on the transaction being examined. In a fully interactive system, rising prices might actually result in higher demand (in anticipation of a shortage, for example) but to explain principles we hold all other elements the same to focus our attention on how just one element works. We will use the code [CP] as an abbreviation.

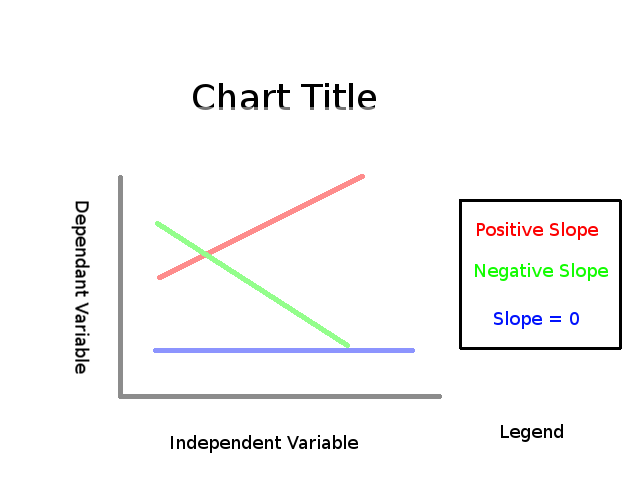

This covers everything in the first meeting of my class, apart from a few drawings on the board. They included examples of several types of Graphs or Charts (line, bar, pie, scatter), the concept of Slope (how much the Dependent variable changes when the Independent variable changes and which direction), Maximum, and Minimum (on charts). The key parts are shown on the following picture.

Chart Examples for Lesson 02

Next time we start on Choice, Opportunity Cost, and Specialization!

Phred

post 69 of n